The Beginnings of Institutional Ethereum: Recapping the First Few Weeks of CME Ether Futures

On February 8, CME Group officially launched Ether futures. ETH futures went live just a little more than three years after CME Group began offering Bitcoin futures. In this interview, CME Group Global Head of Equity Index and Alternative Investment Products Tim McCourt discusses the origins of ETH futures, what convinced them that the time was right for the product to go live, how institutional investors’ attitudes towards Ethereum (and crypto as a whole) have changed, and how the response from the market has been.

When did you start thinking about Ether futures?

When it comes to developing new products at CME Group, we really take our cues from customers in terms of what they’re focused on. As soon as we launched Bitcoin futures back in December of 2017, customers were encouraging us to think about Ether in a similar fashion, as it was (and still is) the second largest token by market cap and daily trading volumes. It’s not surprising it was on the fast follower list in terms of customer demand and express interest, but there were a few issues. So we were keeping our eye on it, evaluating it.

We really started to focus in on Ether as a tradable future when we introduced the CME CF Ether-Dollar Reference Rate back in May of 2018. So we introduced an analogous reference rate to the Bitcoin reference rate using ether-dollar fiat transactions from five constituent exchanges – Bitstamp, Kraken, itBit, Gemini and Coinbase — and making sure that the price discovery in the spot market gave us the same comfort level for overlying a futures contract on that market. It took us some time to observe the underlying market, develop the history of the reference rate and then continue to also engage with customers.

It really picked up steam in terms of client interest and feasibility (from our perspective) to introduce a futures contract in 2020. This also parallels the continued increasing interest and enthusiasm around the Ethereum network and decentralized finance and some of the projects that are going on in the marketplace. These things really started to accelerate in 2020 and we kind of hit the tipping point in the latter half of the year in terms of going from the idea phase to the actual launch of the contract.

What sort of criteria were required for CME Group to move from interest to actually launching ETH futures?

Often in the process of validating a new futures product, we reach a crossroads where we need to determine if a particular asset meets various thresholds for offering futures, or if it’s just an interesting market that doesn’t require a futures contract. In order to make that distinction, first and foremost, we want to determine if there is a hedging need.

Next, we examine whether there is a natural, two-sided market for a particular asset. This is important to facilitate, as we have a responsibility as the exchange where these trades take place to offer efficient price discovery and transfer of risk. We continually ask ourselves: will people want to buy and sell this asset at the same time? Can we match buyers and sellers efficiently? Some products are a great idea, but the demand is too one-sided and so it’s hard for us to then build a centralized order book, to facilitate the efficient transfer of risk.

How have you seen attitudes around Ethereum shift among institutional investors?

There is definitely increased enthusiasm around the underlying Ethereum network. I think people continue to be more and more fascinated and excited by the smart contract design elements and what it means for things like DeFi. Then you also look at some of the stablecoin products, many of which use the Ethereum network.

As people have become more accepting of crypto in traditional institutions, they start to look at bitcoin as the first and most popular. And when they start to look at Ethereum, they often discover there are some aspects of the network that might be more palpable for people in terms of how they can use it and what it means for them.

Therefore, there’s more interest in developing projects that then increase the need for managing risk around ether. So, I just think it’s benefiting from that upwelling of enthusiasm, that curiosity and some of the familiarity that bitcoin has already blazed that trail into cryptocurrency. I think people are more comfortable exploring it, both from an institutional perspective or an investment perspective, as well as from a development perspective.

How much is DeFi driving interest?

For people who are in finance, DeFi is a more tactile, palpable adaptation. They’re using some of their familiarity with the way finance works now and looking at potentially better ways to do it with more interesting technology. Whereas there is still a debate around exactly what bitcoin is, people are focusing more on the utility or utilization of the Ethereum network. It seems a bit more accommodating to entrepreneurial development, and I think that’s where it’s less intimidating.

Have people’s familiarity with CME Bitcoin futures helped fuel the adoption of ETH futures?

Yes. It’s worth noting that our introduction of Ether futures coincided with increasing client demand and robust growth in our Bitcoin futures and options markets. While ether may be new to some clients, our futures contract specs and benefits will be familiar to users of our Bitcoin futures – cash-settled, based on the IOSCO-compliant CME CF Ether-Dollar Reference Rate and sized to appeal to a broad array of institution clients and sophisticated active traders.

How are things going post-launch?

When we look at the more anecdotal and direct customer response, it has been really positive. They’re engaged. They’re excited about it. A lot of the participants that are active in Bitcoin futures, whether they’re trading or clearing members, are also now involved in ETH. The enthusiasm level is much stronger around ether in 2021 than for bitcoin in December of 2017, when people were still wrangling with the question of what is bitcoin? What do we do with it? The questions we’re seeing now are more about specific ether strategy vs. bitcoin strategy. Are we investing in both? Do they have differences?

The reaction we’re getting is a little bit more advanced as we’re so much farther along in the history of crypto. It’s an industry that’s here to stay. It’s been adopted by a lot of folks. And now they’re focusing on questions around the size of investment and trading strategies. So, it’s really been great to see.

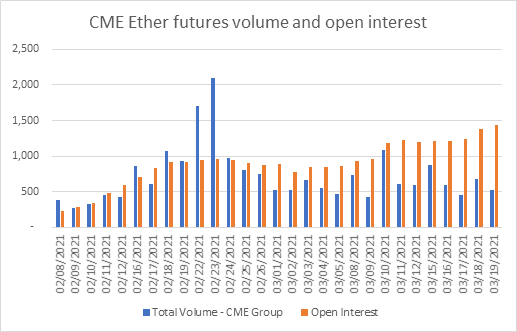

Since their introduction, more than 20.9K CME Ether futures contracts have traded, which is equivalent 1M ether. More than 520 unique accounts have traded the product so far. And, 35% of the volume traded has originated outside the U.S. While it’s still early days, we’re encouraged by these numbers.

Recommended News

-

Bitcoin Exchange LVL Launches Mastercard Debit Card

Upstart cryptocurrency exchange LVL is opening pre-orders for a Mastercard debit card linked to bitcoin and fiat accounts. The card is among Mastercard’s premium products and can be used anywhere globally, said LVL CEO Chris Slaughter. Mastercard did not respond to requests for comment by press time. “It took a couple of months to get [Mastercard] to be comfortable with it being connected to crypto,” Slaughter said. “Convincing them that it was aligned with their premium brand was more involved because their view on crypto businesses is that they’re transactional businesses,…

-

The first year of the blockchain: Consensus Alliance enters the blockchain industry

Blockchain technology is derived from Bitcoin, as people know more about blockchain technology, the blockchain industry is also undergoing great changes. Whether at the level of capital or innovation, blockchain has always been a hot word in 2016. The technical characteristics of distributed general ledger, encryption algorithm and programmability based on blockchain are regarded as the cornerstone of future digital society. Blockchain is expected to lead human society to evolve from information Internet to value Internet. Even, this most subversive technology after the Internet is likely to set off…

-

OEC (OKEXChain)’s first NFT asset aggregation platform Dematrix will be launched on the mainnet soon

The official opening of the third phase of OKEXChain has opened a new era of DeFi ecology, which is good news for everyone in the blockchain world. OKExChain is the world’s first transaction chain-a blockchain technology infrastructure built for transactions. Through the development of “blockchain middleware” and operational support for transaction scenarios, it reduces the development costs of application developers and improves users’ Trading experience. As an open public chain ecology, anyone can campaign to become an OKExChain super node, or they can issue their own digital assets, create their…

-

BKEX Futures Ambassador Recruitment is up!

1.Introduction of BKEX BKEX Global takes product innovation as the core of its development and is committed to promoting the globalization of cryptocurrencies through a diverse, deep and comprehensive derivatives ecosystem. Currently, BKEX Global holds MSB license issued by FinGEN, a subsidiary of the U.S. Department of the Treasury, and has established the BKEX Sunshine Fund to fully protect users’ assets. More than 70% of BKEX technicians are from Microsoft, Xunlei and other leading platforms in the blockchain field. Currently, BKEX has developed technologies such as multi-signature, offline signature, and…

-

Whale Shark’s NFT Collectors Playbook

Thinking about buying some non-fungibles? Maybe you’re even thinking about investing? Maybe you still can’t wrap your brain around the idea of digital art being sold for $69 million, but you’re open-minded, you’ve done your homework and you think the rewards outweigh the risks. And maybe this is money you can afford to lose, so what the hell? [Obligatory disclaimer: Nothing that follows is financial advice. Investing in NFTs – or anything in crypto – is packed with risk and you can lose everything. Proceed with caution.] But if you’re trying to get your…

-

Japan AVF HOLDS HANDS IN SONA TO BUILD NFT ecology

According to official sources, T-power, Japan’s largest AV copyright owner, has announced that it will soon begin creating and releasing NFT copies of SONA and enter into a deal with SONA coinage. Starpunk operating NFT Alliance (SONA) is a decentralized and autonomous organization (Dao) platform, audited by the Soken , and is the heavyweight blockchain authority that audits OpenSea. The no preorder, no private offering by the Geek Coalition of America is the NFT Super Cross chain token, backed by the Andreessen Horowitz Foundation. NETWORK1 aims to connect blockchain/NFT game…

-

Recap of Heroland Community Conference

Heroland Community Conference has successfully ended! Now let’s have a review about the whole conference! Introduction Metaease aims to gather the builders, designers, producers and users of the Metaverse through decentralized autonomous communities and further innovate on the basis of blockchain technology and game production technology, thus build a virtual world that blends with the real world, making it a Metaverse with complete economic cycle and social application value – Metaease will help individuals and organizations stand at the forefront of the future, establish the ultimate expression of the…

-

4JNET is positioned to outperform Safemoon through a unique mechanism

Safemoon launched BSC on March 8, which rose by 200 times within less a month. That is to day, if RMB 10,000 is invested to buy Safemoon in March 3, you will have RMB 2,000,000 in April. It is pointed out that although Safemoon’s price has fallen to $0.000003, the investors may still expose to high risks if they buy Safemoon now. What can Safemoon be used for? The team frankly confessed that it is useless; if there must be one, it takes advantages of a unique mechanism to stimulate people to hoard…

-

OEC (OKEXChain)’s first NFT asset aggregation platform Dematrix will be launched on the mainnet soon

The official opening of the third phase of OKEXChain has opened a new era of DeFi ecology, which is good news for everyone in the blockchain world. OKExChain is the world’s first transaction chain-a blockchain technology infrastructure built for transactions. Through the development of “blockchain middleware” and operational support for transaction scenarios, it reduces the development costs of application developers and improves users’ Trading experience. As an open public chain ecology, anyone can campaign to become an OKExChain super node, or they can issue their own digital assets, create their…

-

Koala Arithmetic Mining Platform: The world’s leading computing power mining platform is officially here

On March 10, 2020, the Koala Arithmetic Mining Platform launched by the Singapore Koala Foundation was officially launched. It is understood that Koala Arithmetic Mining Platform is an innovative global blockchain computing power financial service platform. Its purpose is to redefine the mining industry ecology based on blockchain computing power, and give the platform computing power and The equipment has a certain value liquidity, and finally it will be built into a blockchain computing power financial service platform that integrates computing power services, financial services, circulation services, and information services….