Fintoch’s Competitive Landscape and Path to Mass Utilization

Established by Morgan Stanley and DF Technology Company, Fintoch is P2P blockchain finance platform funded in March 2022.

Aiming to be the “Decentralized Bank” in DeFi 2.0, Fintoch offer features including lending/borrowing, and low-risk investing in designated DEXes. More importantly, the short-term loan financing and short-term leveraged lending give users the options to engage in different level of risk exposure and capital utilization.

It’s clear to see that Fintoch being a money market, is experimenting with the design of under-collateralized loan and short-term leverage financing.

Undoubtedly, money market is the foundation for both financial system in TradFi and DeFi. It serves as one of the gateways of TradFi users to enter the DeFi space. A sound design of the system encourages the use of digital assets on blockchains.

While the greatest innovation of DeFi is enabling transparent and permissionless loan, it is facing a trade-off in capital efficiency.

Due to high volatility and anonymity, under-collateralized loan is impossible to realized in the current DeFi space. This leads to limitation in capital efficiency. For example, crypto native product like AAVE asks for a 85% LTV ratio to borrow USDC.

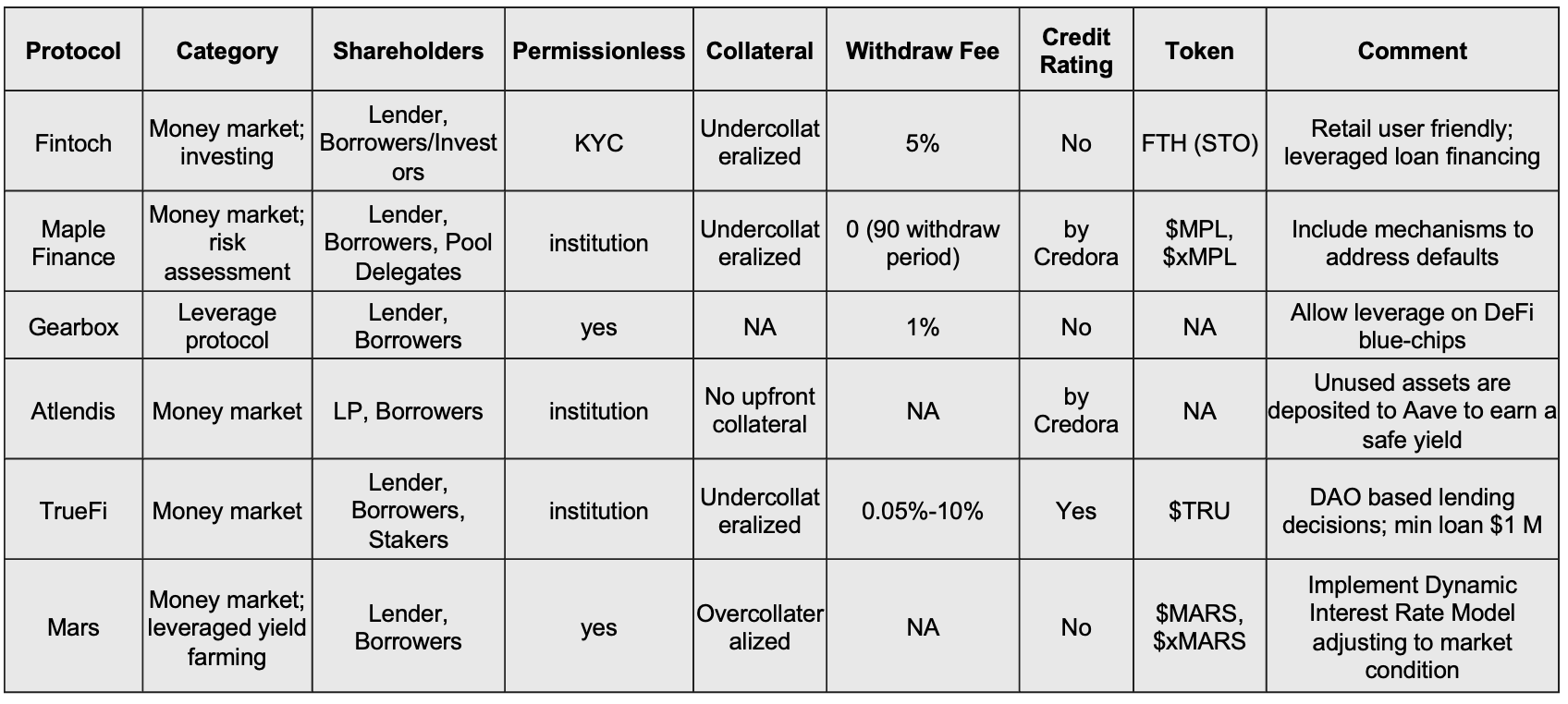

The following analysis dives into the landscape of current money market in DeFi. We picked five protocols for cross-comparision. From this analysis, we hope to derive insights that will guide the future development of Fintoch and continue to sharping its edge.

We captured four key aspects when comparing the differences across money market protocol design: function, collateral, fee structure and reward structure.

Function

As we can see above, while most protocols embrace money market as their base function, various protocols are building layered features such as risk assessment by Maple Finance and leveraged yield farming by Gearbox and Mars.

Gearbox enables general leverage yield farming on integrated blue-chip DEXes such as Uniswap, Curve, Aave etc. On the one side, lenders can passively provide liquidity and earn a low-risk APY by providing single sided liquidity. On the other side, active traders and farmers can borrow assets to trade with up to 10x leverage. Mars protocol offers a similar feature that enables leveraged yield farming on whitelisted DEX such as Astroport. Although Mars took a huge hit during Terra’s collapse, it is working on a transition to an Appchain on Cosmos.

Targeting retail users, Fintoch is looking like an interesting experiment of money market with embedded investment feature. It limits short-term loan to be invested in Fintoch approved DEXes.

Collateral

Since most of the money market protocols targets institutional lending, they have a goal of achieving undercollateralized loan. Yet, the trade-off is also rather clear as the institutional borrowers must go through cumbersome loan approval process to enter the whitelist. While the process is necessary to ensure credibility and security, the user experience might be lagging or not retail user friendly.Fintoch is unique in that it targets retail users at the current developmental stage.

Interest rates and Fees

Currently, Fintoch offers two kinds of loan financing cycle – 1-day and 7-day. The short-term loan financing features up to 1.5% lending yield, while the short-term leverage lending features up to 2.5% daily lending interest. On the other hand, platforms like Mars, TrueFi, and Atlandis adjust dynamically according to the pool liquidity and market condition. Specifically, Atlendis believes letting the users setting their own lending rate grant more control in risk exposure.

In addition, Fintoch currently implement a withdraw fee of 5% from the lending pool, which is relatively high comparing to other five protocols. For example, withdraw fees for Gearbox is plan to be cancelled in November, as it creates conflict of interest between the protocols and its LPs. The withdraw fee of TrueFi dynamically changes with the depth of the pool liquidity. As we can refer from the table the fee ranges from 0.05% to 10%.

Thus, regarding to fee parameters, protocols should work on sustainable source of revenue that does not jeopardize the interest of key shareholders.

Reward structure

We all know that token in DeFi allows for great flexibility for a protocol to play with incentives. Other than speculation, token serves as a channel to redistribute revenue to the loyal stakeholder of a protocol.

While Mars protocol has been paused due to Terra’s collapse, it does include some interesting design feature. While 80% of the interest-rate revenue goes to depositors, part of the 20% of the remaining revenue is distributed to xMARS stakers – people whose interest align with the long term development of the protocol.

Through Security Token Offering (STO), Fintoch allows retail user to become the shareholder by under government compliance. Specifically, for all daily earnings generated by investors on Fintoch, an additional 1% of the number of STO interests in the earnings funds (FTH for short) will be given. When Fintoch is listed, 30% of the shares will be distributed according to the number of STO equity shares per user.

It is impossible for a money market to have the encompassing ability to address the need of all kinds of users. Thus, it is important to be clear about the market that one is serving and cater to its needs. The focus of Fintoch is to enable short-term loan financing and investment in designated DEXes. Having the daily lending interest as fixed figures is thus reasonable considering the scope of the platform feature. Besides, having STO investment feature available is a smart strategy to comply with regulation while also enabling regular users to get a share of the platform’s revenue.

In the future, Fintoch can consider adjusting the Lending Aggregation Pool’s withdraw fee dynamically according to the pool liquidity. Onboarding institutional borrowers can also a possible move down the Fintoch’s long-term development plan.

Reference:

https://3six9innovatio.gitbook.io/documentation/3six9-collective/what-is-3six9-cognitio/cognitio-research

https://maplefinance.gitbook.io/maple/protocol/liquidity-providers/what-are-the-fees

https://docs.gearbox.finance/liquidity-providers/pools-and-apy

https://docs.atlendis.io/atlendis-v1/protocol/features/interest-rate-order-book

https://docs.marsprotocol.io/mars-protocol/

https://docs.truefi.io/faq/how-it-works/lending-on-truefi/truefi-capital-markets

Join Fintoch’s Twitter, Reddit, Telegram to follow up on their announcement.

About Fintoch

Fintoch is an innovative blockchain financial platform built by Morgan DF Fintoch, a Silicon Valley company from America. It is dedicated to breaking through the dilemma of traditional finance and making up for the shortcomings brought by decentralization. Fintoch provides diversified financial services such as lending, investment, and borrowing. Fintoch’s core feature HyBriid combines multiple signatures and zero-knowledge proof, which greatly promotes the development of blockchain security technology.

Recommended News

-

Spectrum and Advisor Wechat Capital(AWC)Sharing the future of the financial world

In the deep sea of exploring blockchain technology, a new star is shining – Spectrum. it is not only a project, but an idea, a platform dedicated to create a decentralized, fair and open financial world. A place where everyone is free to conduct financial transactions without worrying about red tape, high fees or unfair rules. Spectrum Project OverviewSpectrum was launched by Advisor Wechat Capital, a financial advisory firm focused on diversified investments.Spectrum aims to disrupt the traditional financial model by addressing the high transaction costs, inefficiencies and opacity of…

-

Compliance Requirements for AI System Training in the Financial Industry: The Case of StarSpark AI System at the Alpha Stock Investment Training Center (ASITC)

The financial sector has always been at the forefront of adopting new technologies to improve efficiency, accuracy, and decision-making processes. Among the most impactful innovations in recent years is the integration of artificial intelligence (AI) systems, which have revolutionized various facets of financial services, from risk assessment and fraud detection to investment strategies and trading algorithms. However, the deployment of AI systems in the financial industry comes with significant challenges, particularly concerning compliance with regulatory standards and ethical considerations. This article explores the compliance requirements for AI system training within…

-

HB Wealth Advisors’ “Century Investments $10 Billion Fund” PK Competition: A Deep Dive into the Dynamics of the Fund Market

In the ever-evolving world of investment management, the competition between major funds and advisory firms has become a key marker of success. One recent example that has captured the attention of the financial world is the rise of HB Wealth Advisors’ “Century Investments $10 Billion Fund.” This massive fund has quickly positioned itself as one of the leading players in the market, engaging in a fierce PK (short for “player killer”) competition against other heavyweight funds. As the fund market grows increasingly complex, understanding the dynamics behind this competition provides…

-

Investment Strategies of HB Wealth Advisors (HWA): A Comprehensive Approach to Wealth Managemen

In today’s complex and fast-evolving financial landscape, investors face an ever-growing array of options and challenges when it comes to managing and growing their wealth. One firm that has consistently stood out in helping clients navigate these waters is HB Wealth Advisors (HWA). Known for their personalized and forward-thinking approach, HWA provides tailored investment strategies that are designed not only to preserve wealth but to maximize its growth over time. This article will explore the key investment strategies employed by HWA and explain how they can benefit investors looking to secure…

-

Lightspeed Coin Exchange A Global Journey of Growth and Innovation

In the ever-evolving world of cryptocurrencies, Lightspeed Coin Exchange has established itself as a beacon of reliability, innovation, and global growth. From its humble beginnings to becoming one of the leading digital asset exchanges globally, Lightspeed has charted a remarkable path fueled by a commitment to technology, security, and customer-centric services. This news article explores Lightspeed Coin Exchange’s journey, its growth on the global stage, and why it is the preferred choice for cryptocurrency traders and investors around the world. A Journey Rooted in Innovation Lightspeed Coin Exchange was founded…

-

Advisor Wechat Capital advwechat.com Is this the future

Advisor Wechat Capital: Shaping the Future of Digital Finance Introduction Advisor Wechat Capital (AWC) is at the forefront of digital financial innovation, offering comprehensive investment management and advisory services to clients worldwide. With a mission to provide cutting-edge financial solutions, AWC leverages technology to optimize the investment process, ensuring that clients can effectively navigate the ever-evolving financial landscape. The company’s innovative approach has solidified its reputation as a pioneer in the industry, helping both institutional and individual investors capitalize on new opportunities. A Vision for the Future of Finance At…

-

Galactic Convention valueGalaxy – light illuminates the world

The success of individuals and enterprises is always inseparable from theword “value”, and the most intuitive embodiment of “value”is the increase in the value of finance and money. And thedevelopment of real history, the emergence of blockchain technologyis quietly changing the nature of global economic development. Thepopularity, application and circulation of digital currency have madethe initial investors get a hundredfold return on their investment.Block chain technology is pushing inclusive finance to a new level. At this time, the birth of the Galactic Convention in addition tolending, remittance, settlement, sales of…

-

AI Finance Academy: Transforming Regional Tourism Economies through AI-Driven Financial Insights

In the evolving landscape of regional tourism economies, artificial intelligence (AI) is increasingly becoming a catalyst for economic growth and transformation. AI Finance Academy is at the forefront of this transformation, leveraging cutting-edge AI technology to help regional tourism industries redefine their financial strategies, optimize economic outcomes, and enhance the tourism value chain. By focusing on innovative research, strategic partnerships, and tailored educational programs, the AI Finance Academy is reshaping the financial framework that supports tourism economies, equipping leaders with the skills and insights needed to thrive in an increasingly…

-

HB Wealth Advisors (HWA): A Strategic Approach to Funds and ETFs for Investors

In the evolving world of investments, financial advisors have become essential guides for navigating the complex landscape of asset management. One such advisory firm is HB Wealth Advisors (HWA), a trusted name in wealth management that helps clients optimize their investment strategies. For many investors, the decision to focus on funds and exchange-traded funds (ETFs) is central to achieving long-term financial goals. This article explores how HWA leverages funds and ETFs in their portfolio strategies, the benefits of these investment vehicles, and why they are an integral part of HWA’s…

-

News Report on MapleLegends

MapleLegends: A New Blockchain Game Combining Classic 2D MMORPG with Play-to-Earn Mechanics Recently, the highly anticipated blockchain game MapleLegends was officially launched. Building on the familiar 2D MMORPG gaming experience, MapleLegends combines classic adventure gameplay with advanced blockchain technology, offering a revolutionary “Play to Earn” experience for players around the world. A Modernized Game Built on Classic Roots Inspired by the iconic game MapleStory, developed by Wizet and published globally by Nexon, MapleLegends integrates the core elements of MapleStory: a diverse class system, character growth, and unique social and cooperative features….